The IT services sector in Australia has become private equity (PE) investors’ new hunting ground, offering favourable conditions for a typical PE roll-up play, according to industry experts.

The latest on the block is Melbourne-based Interactive, which, as reported, has engaged Rothschild to seek an equity partner to back an M&A-fuelled growth strategy. If Interactive ends up partnering with PE, it would be following a well-trodden path led by recent transactions in the sector.

In December Adamantem Capital completed the acquisition of a majority stake in Nexon AsiaPacific, sold by EQT; the same month saw Brennan IT securing strategic investment from MacquarieGroup’s principal investment arm, which, although not a standard PE transaction, is still a financial sponsor-backed deal; in October, Advent Partners bought a majority stake in Efex. Deal financials were not disclosed.

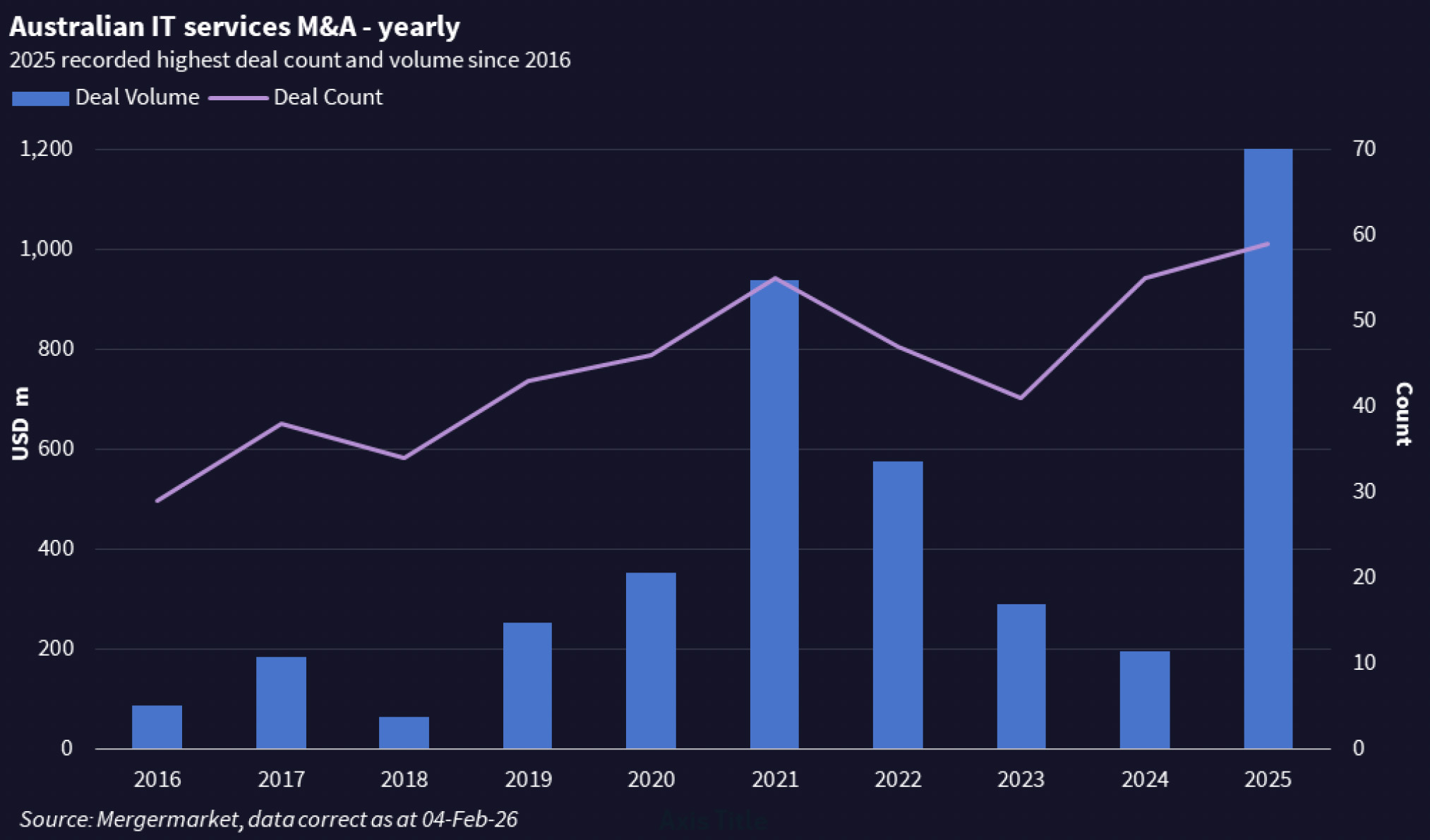

According to Mergermarket data, Australia’s IT services sector recorded 59 deals in 2025 with a total volume of USD 1.2bn (excluding deals that did not disclose volume), rising from the previous year’s55 deals with a total volume of USD 196m. Notably, sponsor-backed activity in the sector has picked up pace in recent years to reach 22 deals in 2025, the highest count ever.

“In recent three years there has been an emergence of strong PE interest in IT services,” said Mark Nesbitt, principal of Latimer Partners, a technology-focused M&A advisory firm based in Sydney. “Almost all the PE firms we are talking to are looking for IT services targets.”

The surge of PE interest in IT services is largely thanks to four factors: the sector still has plenty of growth, is highly fragmented, while IT services companies are “people businesses” and are profitable, according to Pierre Briand, founder of Sydney-based SCF Advisory.

“These are perfect elements for PE,” he said. The fragmented sector means there is opportunity forPE backers to do roll-up, while PE also knows how to manage people incentives and successions, Briand elaborated.

Both Nesbitt and Briand added that the sector’s profitability and regular revenue also allow PE sponsors to put some leverage.

Adamantem, for its part, sees a lot of opportunity in the managed IT services sector for leading providers like Nexon, according to managing director Katie Wood, citing strong tailwinds including client IT environments becoming more complex, clients continuing to invest in digital transformation and increasing demand for stronger cybersecurity. The fragmented market also provides “an attractive context for Nexon to pursue strategic acquisitions that add scale and new capabilities,” she added.

Pacific Equity Partners also spotted the opportunity there as it bid against Adamantem for Nexon, as reported.

PE vs strategic buyers

PE interest in Australia’s IT services seems to have been sparked by Quadrant Private Equity’s Arqdeal in 2022, Nesbitt said. As per Mergermarket data, Quadrant carved out Arq from a parent company of the same name in February 2020 through its inaugural growth fund for an entry valuation of AUD 35m and in just two years sold the business to NCS Group, a SingTel Group-ownedIT and communications engineering company, for AUD 290m.

Briand pointed to an earlier deal - Adamantem’s exit of Servian to NASDAQ-listed Cognizant in 2021after having owned a majority stake since June 2018. These deals, both generating great returns for investors, served “as a testimony” to PE’s approach on IT services targets, he said.

Prior to the emergence of PE interest, M&A activity in Australia’s IT services was driven by serial acquirers listed on the ASX, Nesbitt said.

The difference, according to the advisor, is that strategic buyers tend to see things from bottom up -“if they see there is a capability gap in their own services, they go out to buy a business to plug the gap” - while PE buyers tend to be “thematic investors” that see the tailwinds for the sector and then do research and find the right target.

“PE buyers usually show a lot more rigour and discipline in target search, while strategics often assume they know the sector well,” said Nesbitt, who usually works on the sell-side. PE is also adept at executing roll-up, usually with a clear vision about the targeted scale of the business both in terms of financials and products, he said.

Strategic buyers offer synergy opportunities but are “a bit risk-averse” now, while PE buyers are risk-takers and more agile, Briand said, adding that PE buyers know how to structure an IT services deal that usually includes earn-out arrangements.

PE buyers sometimes over pitch their industry knowledge in dealing with potential IT services targets, according to Briand, who usually works with privately owned businesses. “Instead they should pitch what value they can bring to the business, (such as) how they can renew the board, find good executives, reshape the business, support inorganic growth,” he said.

Attractive categories

The usual playbook is to start with a platform asset and then plug in more capabilities through bolt-on acquisitions. However, it is not easy to find a good platform asset that ticks all the boxes: the right management, the right size, profitability and growth opportunities, said Briand, who has worked with both platform asset targets and roll-up asset targets.

In 2025, SCD Advisory advised on the sellside for Dyflex in the sale to Five V Capital as a PE platform asset and for Libertas in the sale to Tambla Business Services, backed by private equity fundLiverpool Partners (LVP), as a roll-up asset.

The most attractive businesses in IT services are managed service providers (MSP), SAP andMicrosoft partners, data analytics, cyber security services providers, while AI is still more for venture capital (VC) investment at this stage, he said.

Nexon, Brennon IT, Efex, and Riverside-backed Virtual IT are in the category of MSPs, which will drive continued consolidations in the sector as “this will automate the back office and free up owners’ time to allow them drop the boring stuff and focus on things they enjoy doing”, said Nesbitt.

Companies like Quadrant-backed Arinco are in the category of Microsoft partners, he noted. Since 2022, Quadrant’s Growth Fund No.2 has partnered with Arinco, Cevo, an AWS partner, as well as D6 Consulting to form a group of Australia’s fastest growing cloud services providers called Connetico.

Cyber security is another space that has seen increased PE interest and roll-up activity, showcased byQuadrant’s investment in Bastion in 2023, Pemba in ctrl:cyber (2024) and Five V in Penten (2021).Last year BGH Capital sold CyberCX, which is a roll-up of about 20 acquisitions, to Accenture for reportedly more than AUD 1bn.

Size matters

In terms of target size, targets with only 20-30 staff will be too small for PE to look at. “AUD 5-AUD 10m EBITDA is the bottom line for PE to take a look, or AUD 30m-50m revenue will start to be interesting,” Nesbitt said.

EBITDA of AUD 20m-AUD 25m would be a “magic” figure for PE investors – they can either invest or grow businesses to that level and then seek to exit to larger players, he added.

Another banker who has been approached to look at IT services cautioned that people are tempted to pitch IT services as software and tech businesses and expect to get similar valuation multiples in the high teens or even early twenties of EBITDA. However, this is fundamentally a professional services business that relies heavily on people and may not justify such multiples, the banker argued.

PE owners of IT services companies are most likely to exit to another sponsor or strategic buyer, while the IPO window for such businesses is still closed, according to Nesbitt. “The valuation on the public market is just not there to be appealing,” he added.

Strategic buyers active in Australia’s IT services space last year include some large multinational players – apart from Accenture, India’s Infosys bought a 75% stake in Versent, a Telstra subsidiary, for AUD 233m and The Missing Kink for AUD 98m, while NASDAQ-listed Insight Enterprises bought cyber security services provider Sekuro for an undisclosed amount.

Following Nexon, another sponsor-backed IT services company on the market now is LVP-owned Orro Group, which has appointed Houlihan Lokey to find a buyer. According to a report in the Australian Financial Review, Orro may be presented to trade buyers including Japanese telcocompanies.

For future investors, one key risk or opportunity for IT services is the impact of AI, Briand said. “WillAI be an opportunity for growth, for efficiency, productivity, cost cutting, or will AI be disruption? It is still an open question.”

by Maggie Lu Yueyang, with analytics by Manu Rajput